What is worse than a decline?

Being tied up in red tape is what is worse !

I had some new clients come in last month and I would call the loan structuring they were set up with by their bank a Big Mess! Capitals! Why? All three properties and all three loans were cross collateralized. They wanted to sell one property and move to the coast, but without a specialist to untangle this contractual mess, they were stuck.

Being tied up in red tape is what is worse !

I had some new clients come in last month and I would call the loan structuring they were set up with by their bank a Big Mess! Capitals! Why? All three properties and all three loans were cross collateralized. They wanted to sell one property and move to the coast, but without a specialist to untangle this contractual mess, they were stuck.

What is it?

It is where the bank or lender will secure one loan with more than one property in order to improve it’s equity position. In effect, the bank sinks it’s claws into as much property as it can, on as many loans as it can. I use this term because in most cases it is unnecessary. Also, banks aren't inherently being 'bad guys' it is just sometimes the old school way of doing things, and completely unnecessary in this day and age in most situations.

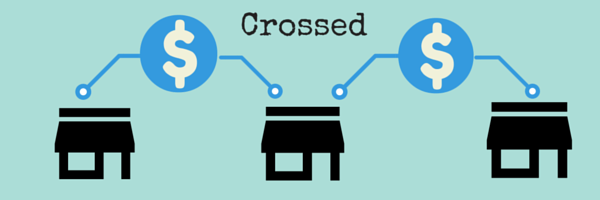

In the graph below, the loans represented as $ are mortgaged to the houses attached by lines. In this example, two mortgages are cross collateralized against three properties. To sell one property, the bank must revalue the related mortgaged property. From here the bank will determine how much they want the mortgage reduced by the sale.

It is where the bank or lender will secure one loan with more than one property in order to improve it’s equity position. In effect, the bank sinks it’s claws into as much property as it can, on as many loans as it can. I use this term because in most cases it is unnecessary. Also, banks aren't inherently being 'bad guys' it is just sometimes the old school way of doing things, and completely unnecessary in this day and age in most situations.

In the graph below, the loans represented as $ are mortgaged to the houses attached by lines. In this example, two mortgages are cross collateralized against three properties. To sell one property, the bank must revalue the related mortgaged property. From here the bank will determine how much they want the mortgage reduced by the sale.

Can it be avoided?

Yes! With the help of your mortgage broker, you can choose to split your loans so that they are all ‘stand alone’. I.e. if you need equity out of your home to buy an investment, simply take out the deposit and costs as an equity loan, separately, that is only secured by your home. Then, take out an investment home loan against the investment property. You’ll end up with two loans but as both were used for investment both are tax deductible. When it comes time to sell your home or the investment, you will know exactly which loan needs to be paid off. If you cross collateralsed however, the bank can hold one property ransom to the other, demanding that you pay down debt other linked loans! I have seen this nearly bankrupt people in falling property value markets.

In one particular case, I saw a bank try to force their hand claiming that the loans were cross collateralized. I investigated for the client and found they were stand alone, thus releasing the clients from a near fatal financial blow. This is the difference between someone who is an expert at structuring mortgages, and someone that isn't, or simply chooses not to care for your financial well being.

The below graph illustrates a nice neat 'stand alone' mortgage structure, avoiding all the pitfalls of crossed securities. If any of these properties were to sell, the mortgagor would only need to pay off the linked loan/s. There is no confusion down the road, and no obstacles to refinancing individual home loans.

Can it be avoided?

Yes! With the help of your mortgage broker, you can choose to split your loans so that they are all ‘stand alone’. I.e. if you need equity out of your home to buy an investment, simply take out the deposit and costs as an equity loan, separately, that is only secured by your home. Then, take out an investment home loan against the investment property. You’ll end up with two loans but as both were used for investment both are tax deductible. When it comes time to sell your home or the investment, you will know exactly which loan needs to be paid off. If you cross collateralsed however, the bank can hold one property ransom to the other, demanding that you pay down debt other linked loans! I have seen this nearly bankrupt people in falling property value markets.

In one particular case, I saw a bank try to force their hand claiming that the loans were cross collateralized. I investigated for the client and found they were stand alone, thus releasing the clients from a near fatal financial blow. This is the difference between someone who is an expert at structuring mortgages, and someone that isn't, or simply chooses not to care for your financial well being.

The below graph illustrates a nice neat 'stand alone' mortgage structure, avoiding all the pitfalls of crossed securities. If any of these properties were to sell, the mortgagor would only need to pay off the linked loan/s. There is no confusion down the road, and no obstacles to refinancing individual home loans.

Further benefits are that if you require lenders mortgage insurance, because your equity is low, stand alone structuring will result in a considerably smaller premium. That saves thousands when we compare scenarios for our clients, to helps to better understand good loan structuring.

All the loans can be split by purpose for your accountant too, to make tax time easier. Further you can have greater control over where your surplus funds are going and which loans are being paid off faster. Preferably the rule is the non-tax-deductible ones!

Suffice to say our new clients have now removed two investment properties from their own home, thus relieving a great deal of stress and ensuring that their 'castle' is safer.

All the loans can be split by purpose for your accountant too, to make tax time easier. Further you can have greater control over where your surplus funds are going and which loans are being paid off faster. Preferably the rule is the non-tax-deductible ones!

Suffice to say our new clients have now removed two investment properties from their own home, thus relieving a great deal of stress and ensuring that their 'castle' is safer.

RSS Feed

RSS Feed