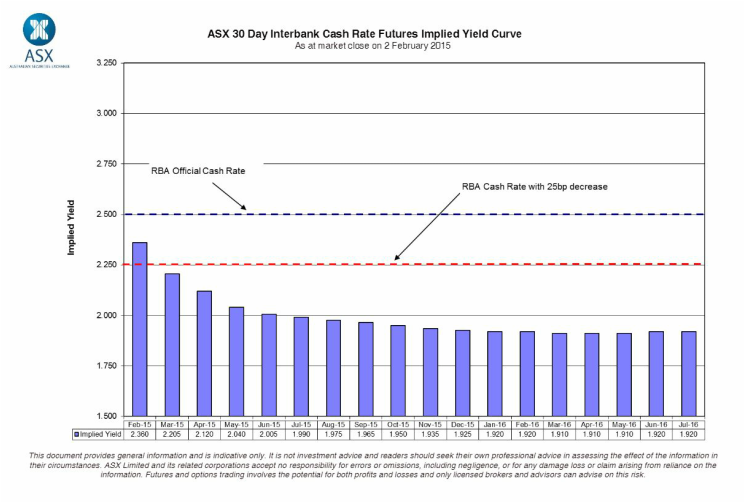

Cash Rate Futures (below) provide an exact measure of market expectations for the official cash rate over the next 18 months. The implied probability of changes in the cash rate can be calculated from these expectations. On current pricing, the RBA is seen cutting rates by 25bps by April with a further 25bp cut to be delivered by the end of the year.

Expectations for further monetary policy easing will bolster confidence in property markets, giving further uplift to house prices and encouraging investors to stay in the market a while longer in light of cheaper lending rates. Concern about the impact of rate hikes on the housing market had been weighing on price growth but have dissipated for the time being as expectations for rates were revised down.

A balanced approach should be taken when weighing up fixed versus variable rates over the next year, as 1 to 5 year term rates remain roughly on par with the variable, tending to imply that banks consider rates are likely to be stable in the medium term.

It's interesting to note that the cash rate is already below the low reached during the global financial crisis, which raises the question of why? Much of the answer has to do with global commodity prices, the impact of collapsing iron ore and coal prices on the mining sector. Weaker prices are accelerating the downturn in resource sector investment and this is dragging on growth while the rest of the economy continues to struggle. The much anticipated transition from mining-led activity to broader-based growth is yet to fully manifest itself and appears unlikely to do so with business and consumer confidence muted.

December quarter inflation figures released this morning provided a partial check on expectations for further rates cuts. Despite the flat headline number, +0.2 per cent in the quarter and just +1.7 per cent over the year, the important underlying measures were firmer than expected and may be signalling a strengthening of inflation over the medium term. The +0.7 per cent quarterly increase in both the trimmed mean and weighted median measures of inflation annualises to a rate of +2.8 per cent and if repeated in the June quarter would raise alarm bells for the Reserve Bank and likely lead to significant revisions to current expectations for cuts to the cash rate.

An interesting regulatory issue to watch this year that will affect anybody seeking finance, is the mooted macroprudential regulations scheduled for late 2015. The exact detail of these changes remains unknown but in the broad these regulations will seek to mitigate risk in the financial system in the whole by constraining bank lending policies. Macroprudential regulations work to limit excesses that can develop during credit booms. Initial speculation is that banks may have their loan to value ratios restricted for instance, capping lending to 90% of values. Since then however, last Friday, APRA announced that nine banks (three of which are big four banks) all fell under their risk indicator. The focus of this report was on investor loan book growth. In response to this the Reserve Bank of Australia has noted that this is fueling additional speculative activity in the market, particularly noting the house price growth is not in line with growth in household incomes. Attempts to stem systemic risk in the banking system will ultimately take the wind out of lending growth. What we see is increasing bank rate competitiveness, other areas for policies to open up to compensate for lending growth, and a general restructure of goal posts for bank credit appetites.

Expectations for further monetary policy easing will bolster confidence in property markets, giving further uplift to house prices and encouraging investors to stay in the market a while longer in light of cheaper lending rates. Concern about the impact of rate hikes on the housing market had been weighing on price growth but have dissipated for the time being as expectations for rates were revised down.

A balanced approach should be taken when weighing up fixed versus variable rates over the next year, as 1 to 5 year term rates remain roughly on par with the variable, tending to imply that banks consider rates are likely to be stable in the medium term.

It's interesting to note that the cash rate is already below the low reached during the global financial crisis, which raises the question of why? Much of the answer has to do with global commodity prices, the impact of collapsing iron ore and coal prices on the mining sector. Weaker prices are accelerating the downturn in resource sector investment and this is dragging on growth while the rest of the economy continues to struggle. The much anticipated transition from mining-led activity to broader-based growth is yet to fully manifest itself and appears unlikely to do so with business and consumer confidence muted.

December quarter inflation figures released this morning provided a partial check on expectations for further rates cuts. Despite the flat headline number, +0.2 per cent in the quarter and just +1.7 per cent over the year, the important underlying measures were firmer than expected and may be signalling a strengthening of inflation over the medium term. The +0.7 per cent quarterly increase in both the trimmed mean and weighted median measures of inflation annualises to a rate of +2.8 per cent and if repeated in the June quarter would raise alarm bells for the Reserve Bank and likely lead to significant revisions to current expectations for cuts to the cash rate.

An interesting regulatory issue to watch this year that will affect anybody seeking finance, is the mooted macroprudential regulations scheduled for late 2015. The exact detail of these changes remains unknown but in the broad these regulations will seek to mitigate risk in the financial system in the whole by constraining bank lending policies. Macroprudential regulations work to limit excesses that can develop during credit booms. Initial speculation is that banks may have their loan to value ratios restricted for instance, capping lending to 90% of values. Since then however, last Friday, APRA announced that nine banks (three of which are big four banks) all fell under their risk indicator. The focus of this report was on investor loan book growth. In response to this the Reserve Bank of Australia has noted that this is fueling additional speculative activity in the market, particularly noting the house price growth is not in line with growth in household incomes. Attempts to stem systemic risk in the banking system will ultimately take the wind out of lending growth. What we see is increasing bank rate competitiveness, other areas for policies to open up to compensate for lending growth, and a general restructure of goal posts for bank credit appetites.

RSS Feed

RSS Feed